What do you mean, Medicare isn’t paying for the nursing home? Families with older loved ones face this shock every day.

Many people learn too late that Medicare does not cover long-term nursing home care. Even when Medicare pays, coverage lasts a short time and includes significant cost-sharing.

Understanding how Medicare pays for skilled nursing facility (SNF) care is critical for proper planning. It is especially important to understand what happens after the first 20 days.

This post explains Medicare nursing home costs and what families can expect after the first 20 days.

Medicare Part A Requirements for Skilled Nursing Care

Medicare Part A may cover care in a skilled nursing facility, but only if the applicant meets several requirements. The most important is the three-day qualifying hospital stay.

The patient must have a formal inpatient admission (not observation status) for at least three consecutive days. From there, they can transfer to a skilled nursing facility for medically necessary care, such as rehabilitation or skilled nursing services.

The observation status versus inpatient admission is critical and often comes as a huge financial surprise for many people. You only find out that Medicare has not covered the nursing home stay after you get a huge bill from the facility.

The First 20 Days With Medicare Coverage

For the first 20 days in a Medicare-covered skilled nursing facility, Medicare pays 100% of the approved costs. The approved costs may include:

- Room and board in a semi-private room

- Skilled nursing care

- Therapy services

- Medications related to the stay

- Necessary medical supplies

For many families, this creates the impression that Medicare will cover everything. Unfortunately, that assumption can become costly.

What Happens to Costs After 20 Days?

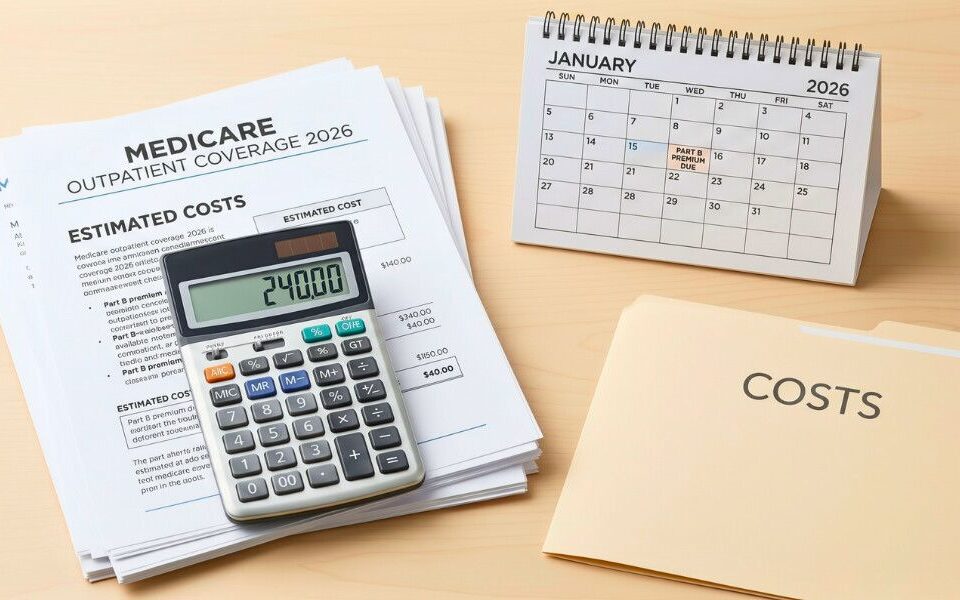

Beginning on day 21, Medicare coverage changes significantly. From days 21 through 100, the patient is responsible for a daily coinsurance payment. For 2026, the co-payment is $214 per day.

While Medicare continues to pay the majority of the cost, this daily charge can add up quickly. An 80-day stay during this period can result in more than $17,000 in out-of-pocket costs.

Some patients have supplemental insurance, such as a Medigap policy or retiree benefits, that may cover this coinsurance. Many do not, and in those cases, the nursing facility will bill the patient directly. Families are often unprepared for these charges because they assume Medicare coverage remains unchanged.

Where Medicare Coverage Stops

Once a patient reaches day 101 of a skilled nursing stay, Medicare coverage for that benefit period ends entirely. At that point, the patient is responsible for 100% of the nursing home costs unless another payer source is available.

For many families, that is when they must make difficult decisions. They must start considering private-pay care, Medicaid eligibility, or alternative care arrangements.

Medicare’s skilled nursing benefit is for short-term rehabilitation, not long-term custodial care. Understanding the 20-day fully covered period is essential.

Families must also learn about what happens after those 20 days. Knowing about the daily coinsurance from days 21 through 100, and the complete cutoff after day 100, will help you plan for care.

The Simple Takeaway

Medicare coverage for skilled nursing can provide much-needed services to seniors. However, families often misunderstand the coverage and eligibility.

The bottom line is simple:

- Days 1 through 20 cost the patient nothing

- Days 21 through 100 require a daily co-payment of $214 in 2026

- After day 100, the patient pays the full cost of care

Knowing these rules in advance is an important step in protecting both health and financial security.

FAQs About Medicare Nursing Home Costs

Does Medicare ever pay for long-term nursing home care?

No. Medicare does not cover long-term custodial nursing home care. It only pays for short-term skilled care when a patient needs medical treatment or rehabilitation after a hospital stay.

What qualifies as a three-day hospital stay for Medicare coverage?

Medicare requires a formal inpatient hospital admission lasting at least three consecutive days. Time spent under observation status does not count, even if the patient stayed overnight. Many families do not realize this difference until Medicare denies skilled nursing coverage.

What costs should I expect after the first 20 days in a Medicare-covered skilled nursing facility?

Starting on day 21, Medicare no longer covers the full cost. Patients must pay a daily coinsurance for each day from day 21 through day 100. For 2026, this co-payment is $214 per day. After 100 days, all costs fall to the patient.

What happens if a patient improves but still needs help after skilled care ends?

Once skilled services stop, Medicare coverage usually ends, even if the patient still needs daily assistance. Ongoing help with activities such as bathing, dressing, or supervision counts as custodial care, which Medicare does not cover.

How do families usually pay for care after Medicare stops?

Common options include private pay using savings or income, long-term care insurance, or Medicaid for those who qualify. Each option has different rules and financial consequences, which is why early planning is important.

When should families start planning for Medicaid or long-term care options?

Ideally, planning should begin before Medicare coverage ends. Waiting until a large nursing home bill arrives can limit choices and increase stress. Early guidance helps families understand eligibility rules and avoid costly mistakes.

Start Planning Your Long-Term Care Options Today

Do you need help with long-term care planning in Florida? Reach out to the Scott Law Offices for assistance. We can help you navigate Medicare and Medicaid rules to ensure you understand your options.

{kind=link}

{kind=link}